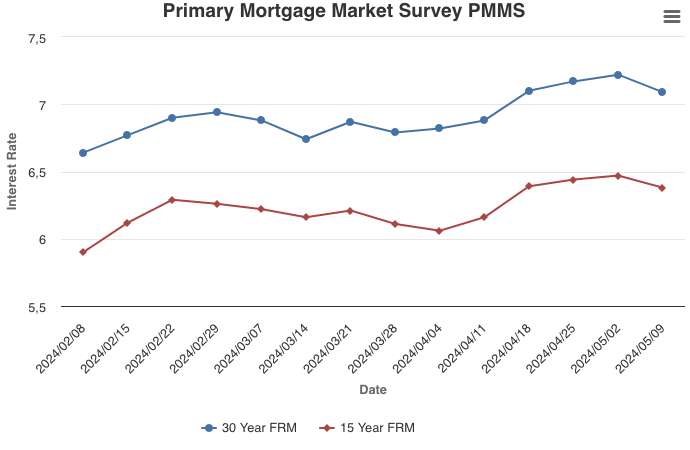

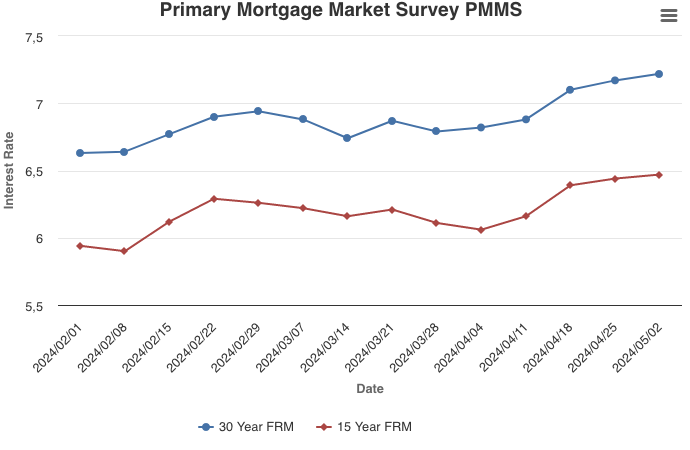

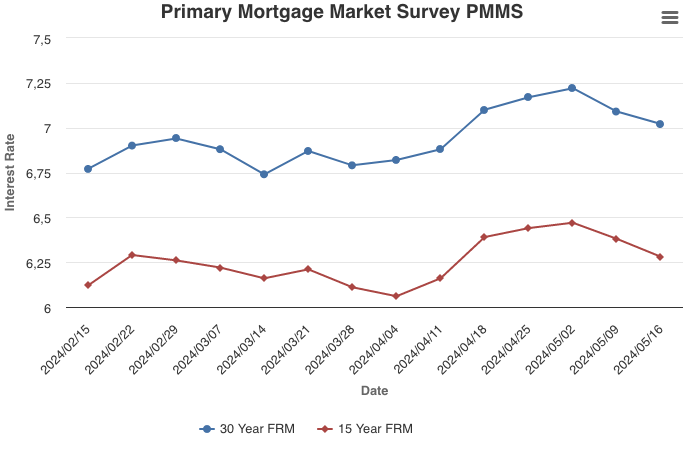

May 16, 2024

Mortgage rates decreased for the second consecutive week. Given the news that inflation eased slightly, the 10-year Treasury yield dipped, leading to lower mortgage rates. The decrease in rates, albeit small, may provide a bit more wiggle room in the budgets of prospective homebuyers.

Information provided by Freddie Mac.

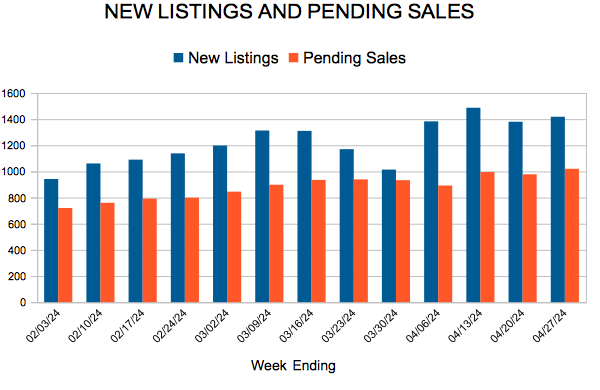

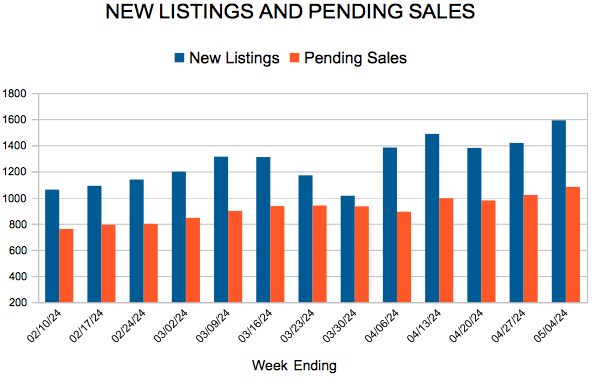

For Week Ending May 4, 2024

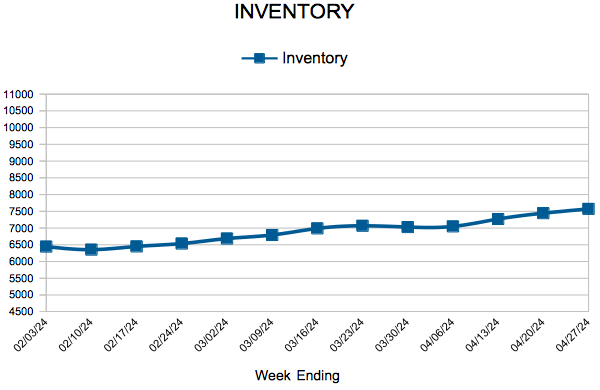

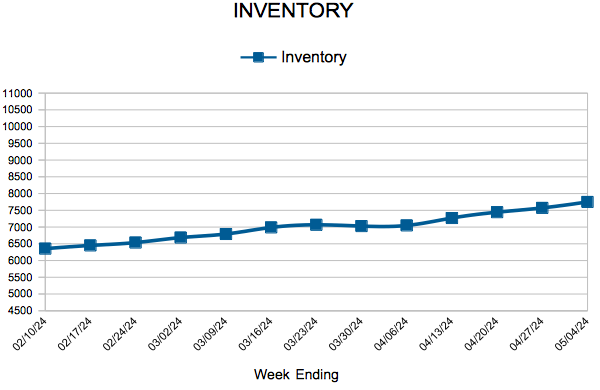

For Week Ending May 4, 2024